Manhattan Real Estate Market Report: Q4 2024

The Manhattan real estate market in the fourth quarter of 2024 displayed a complex mix of trends across various property segments, highlighting both opportunities and challenges. The market’s overall dynamics reflected a shift influenced by macroeconomic factors such as interest rates, consumer sentiment, and economic recovery. While price adjustments were evident in several areas, increased sales activity and tightening inventory levels signaled a gradual move toward balance. Each segment of the market—re-sale, new development, co-op, condo, and luxury—exhibited unique characteristics, underscoring the diversity and resilience of Manhattan’s real estate landscape.

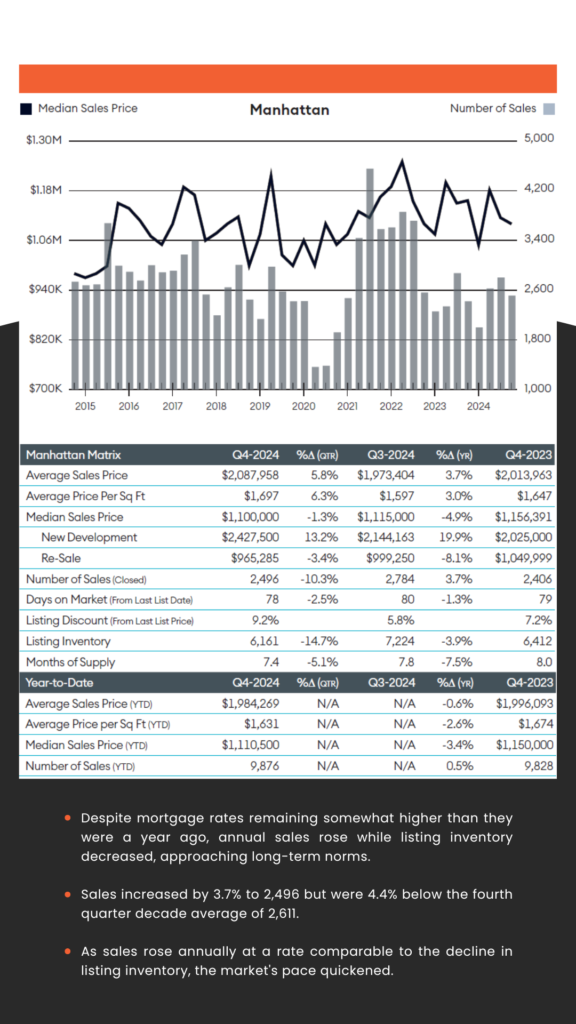

Manhattan Market Overview

The median sales price decreased by 4.9% year-over-year to $1,100,000, indicating a softening in property values. The number of sales increased by 3.7% to 2,496, suggesting a rise in buyer activity despite declining prices. Listing inventory fell by 3.9% to 6,161, reflecting a tightening supply in the market. The months of supply decreased by 7.5% to 7.4 months, aligning with the ten-year average and indicating a balanced market.

Re-Sales Market

The average sales price for re-sale properties declined by 10.5% year-over-year to $1,720,614, while the median sales price decreased by 8.1% to $965,285. The number of closed sales in this segment rose slightly by 1.4% to 2,138, and listing inventory dropped by 8.1% to 4,970, suggesting increased buyer interest and reduced supply in the re-sale market.

New Development Market

The median sales price for new developments increased by 19.9% year-over-year to $2,427,500, indicating strong demand for new properties. However, the number of closed sales in this segment decreased by 10.3% to 358, and listing inventory rose by 14.7% to 1,191, suggesting a potential oversupply in the new development market.

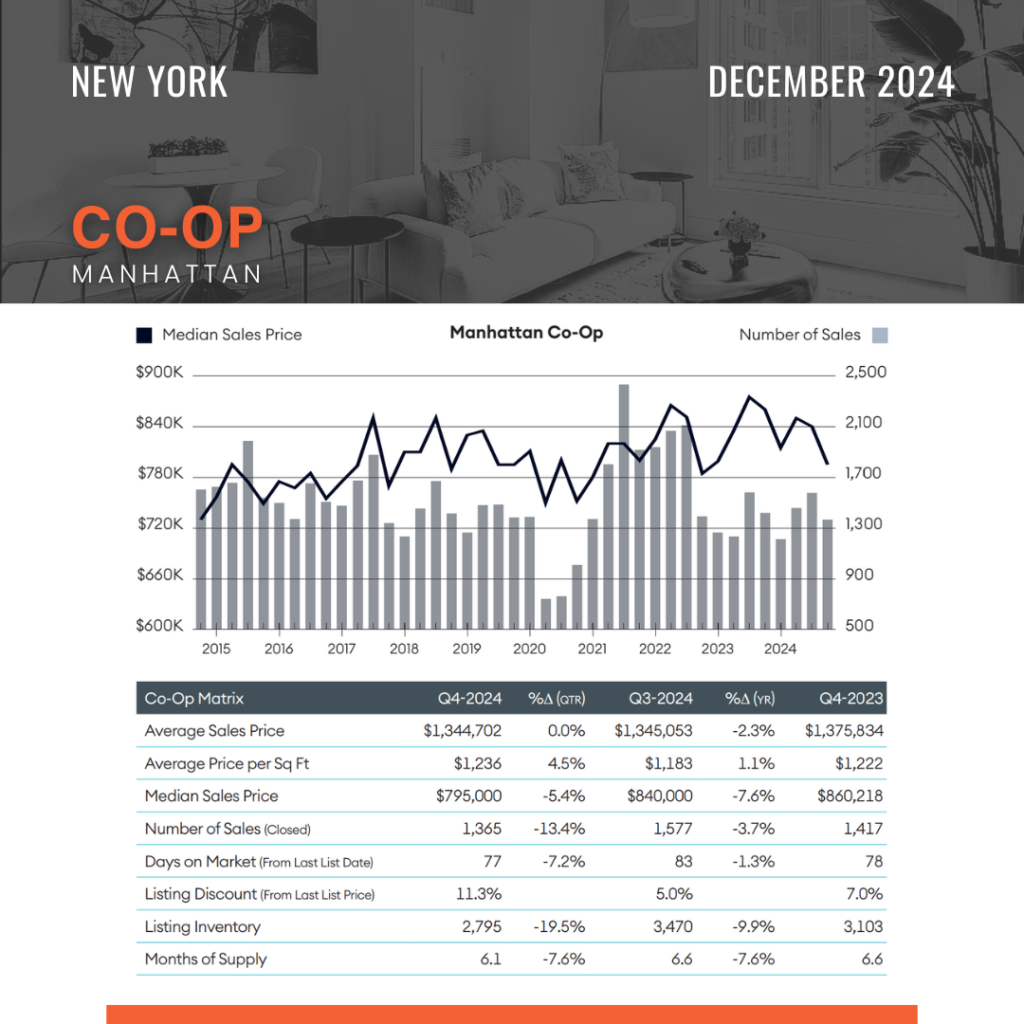

Co-op Market

The median sales price for co-op properties decreased by 5.2% year-over-year to $850,000, while the number of closed sales increased by 2.3% to 1,200. Listing inventory for co-ops declined by 6.5% to 2,800, indicating a tightening supply in this segment.

Condo Market

The median sales price for condos decreased by 4.5% year-over-year to $1,500,000, and the number of closed sales increased by 5.1% to 1,296. Listing inventory for condos fell by 2.3% to 3,361, reflecting a tightening supply in the condo market.

Luxury Market

The median sales price in the luxury segment decreased by 7.8% year-over-year to $5,500,000, while the number of closed sales increased by 4.2% to 250. Listing inventory in this segment declined by 5.6% to 1,000, indicating a tightening supply in the luxury market.

Conclusion

In summary, the Manhattan market demonstrated resilience amidst fluctuating conditions. Declining prices across many segments provided an opening for buyers, while the rise in sales activity indicated a steady demand for properties. Inventory contractions across most categories pointed to a market edging toward equilibrium, even as new developments faced potential oversupply challenges. The luxury market, with its distinct dynamics, reflected the broader market’s trends of adjustment and adaptation. As Manhattan remains one of the world’s most desirable property markets, its ability to navigate these shifts reflects its enduring appeal and flexibility.

About SPiRALNY

Focused on providing a full-service real estate experience, SPiRALNY strives to answer the needs of clients with a sense of detail, care, and efficiency. Our agents work tirelessly to make the process of buying, selling, or renting seamless and exciting.

With an encouraging company culture, cutting-edge technology, and extensive training resources, SPiRALNY agents are destined for success.